When Robert Schiller was awarded the near-Nobel for economics there was also a tacit blessing that the limits of economics as a science were being recognized. You see, Schiller’s most important contributions included debunking the essentials of market behavior and replacing it with the irrationals of behavioral psychology.

When Robert Schiller was awarded the near-Nobel for economics there was also a tacit blessing that the limits of economics as a science were being recognized. You see, Schiller’s most important contributions included debunking the essentials of market behavior and replacing it with the irrationals of behavioral psychology.

Schiller’s pairing with Eugene Fama in the Nobel award is ironic in that Fama is the father of the efficient market hypothesis that suggests that rational behavior should overcome those irrational tendencies to reach a cybernetic homeostasis…if only the system were free of regulatory entanglements that drag on the clarity of the mass signals. And all these bubbles that grow and burst would be smoothed out of the economy.

But technological innovation can sometimes trump old school musings and analysis: BitCoin represents a bubble in value under the efficient market hypothesis because the currency value has no underlying factual basis. As the economist John Quinnen points out in The National Interest:

But in the case of Bitcoin, there is no source of value whatsoever. The computing power used to mine the Bitcoin is gone once the run has finished and cannot be reused for a more productive purpose. If Bitcoins cease to be accepted in payment for goods and services, their value will be precisely zero.

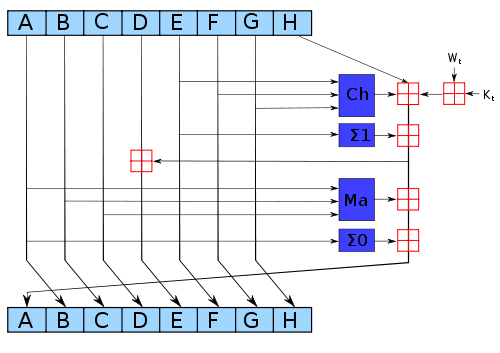

In fact, that specific computing power consists of just two basic functions: substitution and permutation. So some long string of transactions have all their bits substituted with other bits, then blocks of those bits are rotated and generally permuted until we end up with a bit signature that is of fixed length but that is statistically uncorrelated with the original content. And there is no other value to those specific (and hard to do) computations. The only value might be the opportunity costs of spending those compute cycles doing pointless computations, the capital expenditures on mining technology, or the heat generated by the machinery.

So if the BitCoin bubble continues to not self-correct, the efficient market hypothesis is replaced by bootstrapped irrational exuberance for the money, and economics has been reset to the range of cognitive biases that dominates much of our other thinking. That is a science in itself, but it is less an independent economics than had been envisioned by the greats of the field.

This leads us to the question of how to rank the value of specific areas of knowledge for application to real world problems. Applied economic theory remains a hotbed for policy and politics: Does deficit spending lead to economic improvements? How much debt is acceptable? Does economic regulation negatively or positively impact economic growth? Yet if the theory is so porous and incomplete, why should we be so proactive in trying to set policy? Maybe the fallback is individual and group self-interest? Or is the better approach smaller-scale economic experimentation on policy that looks at the effects of targeted changes?